Cell & Gene Weekly

Cell & Gene Weekly

New FDA approved CGT for MLD, and more...

New approved cell therapy alert —> success for Orchard / Kyowa Kirin’s atidarsagene autotemcel (OTL-200), now marketed as LENMELDY (!!!) Enjoy the read and have a good weekend ahead

New FDA approved gene therapy in MLD: LENMELDY

The FDA approved Lenmeldy (OTL-200, a.k.a. atidarsagene autotemcel), a gene-edited cell therapy, for the treatment of children with pre-symptomatic late infantile, pre-symptomatic early juvenile or early symptomatic early juvenile metachromatic leukodystrophy (MLD).

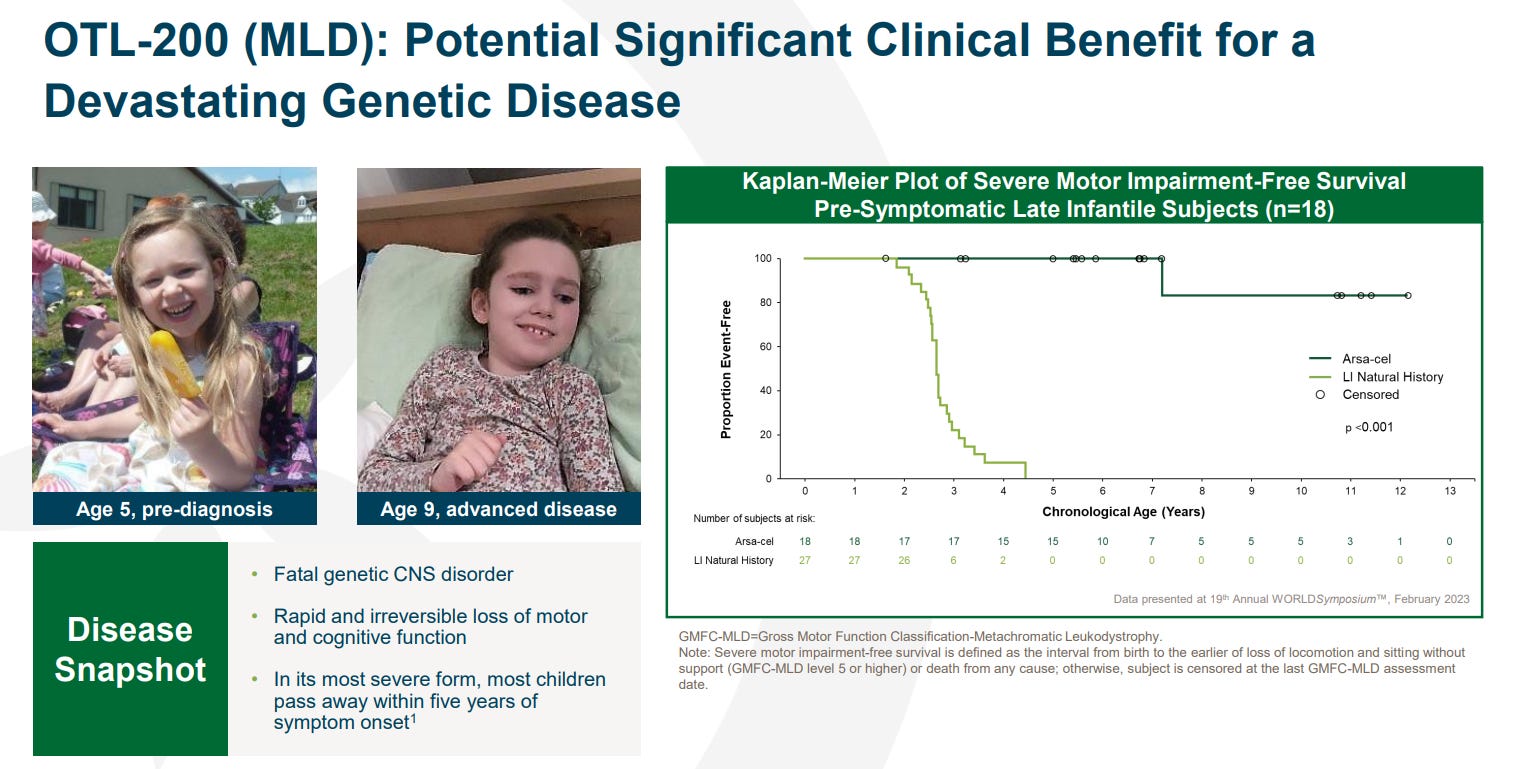

For those that haven’t seen the data, its quite remarkable: treated patients maintained the ability to walk at last assessment in contrast to untreated late infantile natural history patients, all of whom lost all locomotion by a median age of 2.6 years (see KM plot below). Beyond the clinical data, the numerous testimonials of the efficacy of the drug are heartening [CNN, Guardian].

That being said, its going to be an uphill battle for Orchard / Kyowa Kirin: top of mind challenges in my opinion are diagnosis and the pricing & access.

Diagnosis: with an incidence of ~1 /100 k, suspicion of the condition is generally explored only if an older sibling has been diagnosed: and unfortunately for the older sibling, they would be unlikely to be able to access treatment given the therapy is for pre-symptomatic or early symptomatic patients… There’s numerous stories in the news about how younger siblings benefited from the therapy whilst the older ones suffered the consequences of the horrible disease …

Pricing: headlines so far have put significant emphasis on the wholesale price of $4.25 M, (understandably so). As always, it is important to put into perspective the price point: a one-time gene therapy is the equivalent of buying a house (vs renting it for life = chronic treatment), so high upfront cost is not necessarily “expensive”. That being said, Orchard / Kyowa Kirin did price the therapy above the $3.9 M top-end threshold determined by ICER in their evaluation. There will be value based agreements and discounting, but certainly the price point is on the higher end of the estimated range.

This brings to light a fundamental challenge relating to return on investment with ultra-rare drug discovery: taking a look at the SEC statements of Orchard from the 2018-2022 period, the spent ~$180 M* in direct R&D expenses in neurometabolic, i.e., Lenmeldy, alongside >$200 M* in other unalocated R&D costs. the >$380M doesn’t account for other costs of running the company, the long term clinical trial + RWE follow up, etc. etc.. With only a handful of patients expected to be treated per year (e.g., in France, HAS estimated maximum of 3 per year), it’ll be interesting to examine the profitability of such therapy.

The positive so far is that payers seem to appreciate the value of the therapy, e.g., in Germany, Libmeldy (the EU name of the therapy) received “major benefit” rating for pre-symptomatic MLD patients , making it one of only five medicines to achieve this (highest possible) therapeutic benefit rating since inception of the Germana AMNOG process in 2011.

Source: fiercebiotech, orchard IR presentation; GBA assessment; AIFA assessment; Haute Autorite Sante HAS

P.S. Those that have been following me for a while know that I like to play a game of understanding the etymology of brand product names. Lenmeldy seems pretty straightforward… LenMeldy = Lentiviral, Meld = MLD

*2018 - acquisition from GSK: $69.3 M in-process R&D charge related to GSK transaction ($87.2 M total for neurometabolic) + other unalocated R&D costs of 14.3 M); 2019 - $39.0 M for neurometabolic+ other unalocated R&D costs of 44.8 M; 2020 - $17.7 + other unalocated R&D costs of 49.2 M; 2021 - $22.4 + other unalocated R&D costs of 40.3 M; 2022 - $28.8 + other unalocated R&D costs of 48.3 M

Interesting insights from Gilead / Kite from their investor day on manufacturing costs

Gilead / Kite held an investor event last week providing a glimpse into their strategy and ambition in cell therapy. Significant emphasis was put on manufacturing, so thought to share one slide that I found particularly interesting on cost improvements and margins: their ambition is to achieve biologics product gross margins of ~80% in the U.S., by 2030 - BOLD (!)

If they are indeed able to deliver, it’ll make for a great case study: don’t think many people believed this would be possible at launch of the first CAR-Ts in 2017.

Source: Gilead

Quick take news

Capstan Secures $175M Oversubscribed Series B with Backing from J&J, Bayer and BMS [source]

[Gene edited] Pig kidney transplanted into living person for first time [source]

Forge Biologics’ Novel AAV Gene Therapy FBX-101 for Patients with Krabbe Disease is Granted UK’s Innovation Passport Designation [source]

CRISPR could disable and cure HIV, suggests promising lab experiment [source]

*Any views and opinions expressed herein are those of the author (Marco Sabatini) and do not necessarily reflect those of his employer

Have I missed anything? Is there something you would like to hear more about? let me know

Great review of the financing inputs for LenMeldy